Investors generally focus on UK smaller company stocks because of their high growth potential. As such their dividend potential often gets overlooked.

Link’s latest annual dividend report for the Alternative Investment Market (AIM) suggests investors may have missed out on some solid income this year by ignoring small caps.

For the first half of 2022, underlying dividends – excluding specials – were up nearly 20% on the year. But factoring in lower special dividends this year, this growth is a more modest 7.4%, to £574 million.

Underlying dividends are now expected to reach £1.09 billion for the whole of 2022, a gain of 13.3% on 2021. That compares to a forecast for £86.8 billion for the whole UK market, a yearly gain of 12.5%. Headline growth is likely to slow because of smaller special dividends this year after a bumper 2021 – growth is forecast to be 2.5% in 2022, to reach a total of £1.22 billion.

In terms of sectors, financial stocks were the largest contributors to the first-half AIM dividend haul, with a gain of 20% on the same period of 2021, returning payouts to pre-pandemic levels. These include asset managers like Impax and Polar Capital, and financial advice firms.

Other strong sectors include industrials, building materials and food and drink stocks – all areas that benefited from the upswing in the economy.

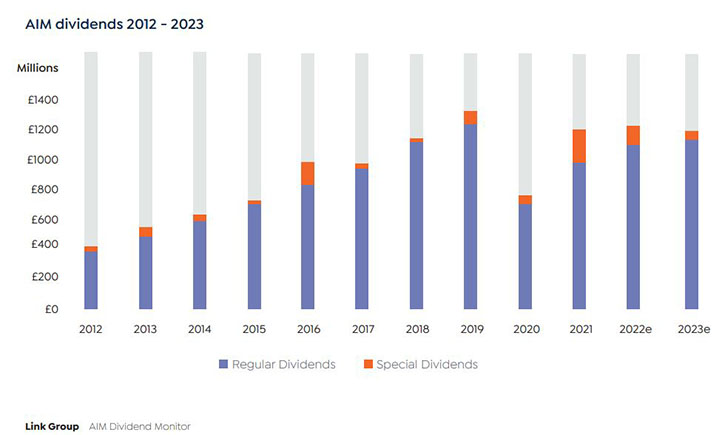

As this is an annual survey, the report also looks at 2021 AIM dividends in total. As with the FTSE All Share, AIM dividends rebounded sharply last year on the pandemic-affected 2020.

Regular dividends hit £962.4 million in 2021, a gain of 39%, while special dividends were up a staggering 331% to £226.3 million. Still, looking at the last 10 years (see chart below), 2019 was the high water mark for AIM dividends – as it was for the main market, where overall income levels have yet to hit their pre-Covid heights.

Cloudy Outlook

Should investors turn their attention to AIM for income? As Link points out, AIM companies are less likely to pay dividends than companies on the FTSE 100 and All Share. So 29% of AIM stocks are expected to make a payout to investors this year, up from 26% in 2021, but more than 75% of main market companies make payouts.

There are some outliers like Rolls-Royce, but recent restorers on the FTSE 100 include Centrica and BT and the overall direction has been broadly positive for the larger caps since 2020. (We cover the latest dividend news for the FTSE 100 in our monthly article.)

This year’s AIM dividend growth can’t obscure the issues faced by UK smaller companies. Ian Stokes, Link’s managing director for corporate markets UK and Europe says of AIM payouts that the “easy work is done” and that growth is now likely to slow.

“We have less visibility on AIM payouts than we do on the more predictable main market but as we move into 2023, we expect growth to slow further,” he says.

“Corporate margins are currently under pressure and a potential recession is on the cards, which will affect both the ability and willingness of AIM companies to return cash to shareholders.

“Underlying dividend growth in the 2-5% range is achievable if the economic squeeze is not too steep, but headline payouts are likely to fall as special dividends are susceptible in downturns.”

Lower Yields

Yields are also lower as you move down the capitalisation scale, with AIM yields forecast to be 1.2% – habitual dividend players pay a higher yield of 2%, but pales against more than 2.5% for FTSE 250 stocks and more than 3.5% on the FTSE 100.

For the first half of 2022, mixer maker Fevertree Drinks was the biggest payer on AIM, handing out £62.2 million to shareholders, with the next being intellectual property firm RWS Holdings with £33.1 million paid out.

Income investors can’t ignore valuations either, and AIM has had a rough ride so far in 2022. Since August 2021, the market cap of AIM companies has fallen £39 billion to £95.5 billion. The FTSE AIM AllShare Index is down nearly 29% this year.

Bigger companies have fared much better due to the value tilt of the FTSE 100 and resurgence of cash generative stocks, meanwhile.

“The UK top 100 index sidestepped the bear, thanks to the dominance of big income-paying multinationals that are prized in an inflationary environment, but AIM hosts hundreds of high-growth companies whose valuation is heavily impacted when bond rates rise, risk aversion spreads and fears of economic recession mount,” the 2022 Link report says.

What is AIM?

The Alternative Investment Market launched 27 years ago in June, 1995, with just 10 companies. There are now under 1,000 companies on AIM, as our explainer reveals.

Regulatory hurdles are lower than for the main London Stock Exchange and many natural resources companies float on the market. Stars include the aforementioned Fevertree (up 428% since 2014), ASOS (up 2,760% since 2001) and Boohoo (down 36% since 2014 but with some strong gains along the way).

There are also plenty of “penny shares” on AIM, which can see staggering returns but stomach-churning falls – I discussed this issue on bargain hunting in my piece, Do Share Prices Matter? If AIM is the home of growth, it can also be the home of huge volatility.

Morningstar generally doesn’t cover AIM stocks as a rule, but ASOS (ASC) falls under our luxury coverage. Analyst Jelena Sokolova thinks the shares are significantly undervalued at their current level, with a 5-star rating.